Your credit score is a three-digit number. But what most Americans don’t realize is that the specific range your score falls into matters more than the exact number — because lenders, card issuers, and landlords make decisions based on tiers, not individual points.

The difference between 668 and 672 is 4 points. But it’s also the difference between “Fair” and “Good” on the FICO scale — and that 4-point crossing can mean a lower interest rate, a higher credit limit, or approval for a card that was previously out of reach.

This guide explains every FICO credit score range in the United States, what each one means for real financial decisions, and how long it typically takes to move from one tier to the next.

Editorial note: CreditPilotUSA.com provides credit education based on FICO scoring methodology. This article is for educational purposes only.

Last updated: March 2026

Quick Answer

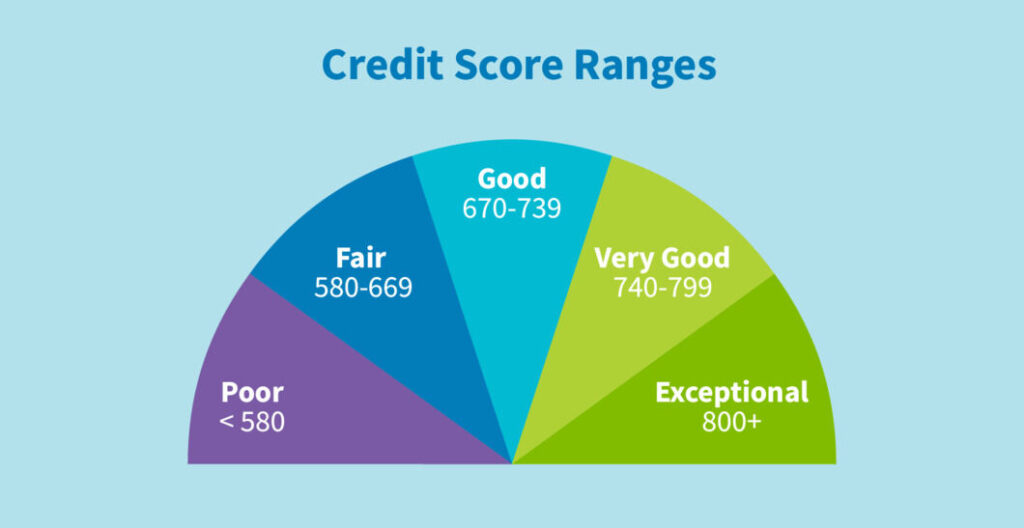

FICO credit scores range from 300 to 850 and are divided into five tiers: Exceptional (800–850), Very Good (740–799), Good (670–739), Fair (580–669), and Poor (300–579). Most lenders use 670 as the informal floor for standard credit products. The best interest rates and premium credit cards typically require 720+. Approximately 57% of Americans have a score of 700 or above.

The Five FICO Credit Score Ranges

800–850: Exceptional

What it means: You are in the top tier of American credit consumers. Lenders view you as an extremely low default risk and compete for your business.

What it unlocks:

- Approval for virtually every credit card, including ultra-premium products

- Best available interest rates on mortgages, auto loans, and personal loans

- Highest credit limits offered by issuers

- Instant approvals on most applications

- Lowest auto insurance rates in states where credit is used for pricing

How common is it: Approximately 21% of Americans have an Exceptional score.

Average FICO behaviors at this tier:

- Credit utilization: under 7%

- No missed payments in the last 7+ years

- Average account age: 9+ years

- Mix of revolving and installment accounts

- Fewer than 3 hard inquiries in the past 24 months

How to get here from Very Good: At 740+, the marginal gains come from time and consistency — not from dramatic actions. Keeping utilization under 7% (not just under 10%), maintaining perfect payment history, and allowing the average age of accounts to grow naturally are the primary drivers.

740–799: Very Good

What it means: You are a highly creditworthy borrower. The vast majority of credit products are accessible, usually at near-best terms.

What it unlocks:

- All major rewards credit cards including Chase Sapphire Reserve, Amex Platinum

- Mortgage approval at competitive rates (typically within 0.1–0.25% of best available)

- Auto loans at near-prime rates

- Personal loans with favorable APRs

- Most premium co-brand cards (airline, hotel)

How common is it: Approximately 25% of Americans have a Very Good score.

The gap between 740 and 800: At 740, you qualify for nearly everything. The difference between 740 and 800 is primarily in interest rate pricing — the top-tier rates on mortgages and large loans are reserved for 760+ and 780+ thresholds at many lenders. For credit card approvals, the difference is minimal.

How to move from Good to Very Good: Consistently keep total utilization under 10%, maintain perfect payment history, and allow older accounts to age. Most cardholders move from 700 to 740+ within 12–18 months of consistent behavior.

670–739: Good

What it means: You meet or exceed the minimum requirements for most mainstream financial products. This is the range most Americans aspire to reach during a credit-building journey.

What it unlocks:

- Chase Sapphire Preferred, Capital One Venture Rewards, Amex Gold

- Citi Double Cash, Discover it Cash Back, Chase Freedom Unlimited

- Standard mortgage approval (rates are higher than at 740+)

- Auto loans at standard rates

- Most balance transfer cards

- Personal loans with reasonable APRs

How common is it: Approximately 21% of Americans have a Good score.

The most important threshold in this range: 700. Most issuers use 700 as the informal approval floor for their best no-annual-fee and mid-tier rewards cards. Getting from 670 to 700 typically takes 3–6 months of consistent low-utilization behavior.

Key behaviors at this tier:

- Utilization: typically 10–30%

- Payment history: mostly on-time, possibly one or two older late payments

- Account mix: 2–4 open accounts

- Average account age: 4–7 years

For the best credit cards available at 700, see our credit cards for 700 credit score guide.

580–669: Fair

What it means: You are above the floor of the credit system but below the threshold where mainstream products become reliably accessible. Lenders view you as a moderate risk.

What it unlocks:

- Some unsecured cards (Capital One Platinum, Petal 2, Mission Lane)

- Secured credit cards with better terms and higher limits

- Auto loans — but at significantly higher interest rates (often 8–15% vs. 3–6% at 700+)

- Some personal loans at high APRs

- FHA mortgage eligibility begins at 580 (with 10% down) or 620 (with 3.5% down)

How common is it: Approximately 17% of Americans have a Fair score.

The two most important thresholds in this range:

- 600: First unsecured cards from major issuers become available. See our credit cards for 600 credit score guide.

- 650: First real rewards cards become accessible. The Discover it Cash Back, Chase Freedom Rise, and Capital One QuicksilverOne all open here. See our credit cards for 650 credit score guide.

How long to move from Fair to Good: Cardholders with a 620 score implementing the right strategies — utilization under 10%, no new missed payments, one to two open accounts — typically reach 670 within 9–15 months.

300–579: Poor

What it means: This range signals significant credit risk to lenders. Most mainstream financial products are inaccessible, and those that are available carry very high fees or interest rates.

What it unlocks:

- Secured credit cards (deposit-based, widely available)

- Credit-builder loans

- Some prepaid debit cards with credit-reporting features

- Subprime auto loans (very high APRs — often 18–25%)

How common is it: Approximately 16% of Americans have a Poor score.

What typically causes a score in this range:

- Recent missed payments (30, 60, 90+ days late) in the last 12–24 months

- One or more collection accounts or charge-offs

- Very high credit utilization (60–90%+)

- Thin credit file with no established history

- Recent bankruptcy or foreclosure

The most important threshold: 550. Below 550, the secured card market is your primary tool. At 550+, more options open. See our credit cards for 550 credit score guide.

Realistic recovery timeline from Poor: A cardholder starting at 520 with high utilization as the primary issue (not recent missed payments) can reach 580+ within 60–90 days of reducing utilization to under 10%. If the score is low due to recent missed payments or collections, reaching 580 takes 9–18 months of consistent positive behavior.

The Two Scoring Models: FICO vs. VantageScore

Not all credit scores use the same scale or the same calculation. When you check your score, you may see different numbers depending on the source — and understanding why helps you interpret what you’re seeing.

| FICO Score | VantageScore | |

|---|---|---|

| Scale | 300–850 | 300–850 |

| Used by | 90%+ of lenders | Some lenders; most free monitoring tools |

| Versions | FICO 8, FICO 9, FICO 10 (most common: FICO 8) | VantageScore 3.0, 4.0 |

| Free sources | Experian app, Discover cardholders | Credit Karma, Credit Sesame |

| Medical debt | Included (FICO 8), excluded (FICO 9+) | Excluded (4.0) |

The practical implication: Credit Karma shows your VantageScore — which can be 10–30 points different from your FICO Score in either direction. Neither is wrong; they’re different models. For the score that matters most to lenders, use the Experian app (FICO Score 8) or myFICO.

For the complete guide to checking all your scores for free and understanding which one lenders actually use, see our how to check your credit score for free guide.

What Moving One Tier Can Save You

The financial cost of a lower credit score is real and quantifiable. Here’s what moving from Fair to Good — or Good to Very Good — saves across common financial products:

30-year fixed mortgage ($350,000 loan):

| Score Range | Typical Rate | Monthly Payment | Total Interest |

|---|---|---|---|

| 760–850 | ~6.5% | $2,212 | $446,000 |

| 700–759 | ~6.75% | $2,270 | $467,000 |

| 680–699 | ~6.9% | $2,315 | $483,000 |

| 660–679 | ~7.1% | $2,358 | $499,000 |

| 640–659 | ~7.5% | $2,447 | $531,000 |

| 620–639 | ~7.9% | $2,540 | $564,000 |

The difference between 620 and 760: approximately $118,000 in total interest paid on a standard American mortgage. That is the real financial value of a credit score — not in points, but in dollars.

Auto loan ($35,000, 60 months):

| Score Range | Typical Rate | Monthly Payment | Total Interest |

|---|---|---|---|

| 720+ | ~5.5% | $670 | $5,200 |

| 690–719 | ~7.5% | $700 | $7,000 |

| 660–689 | ~9.5% | $732 | $8,920 |

| 620–659 | ~12.5% | $787 | $12,220 |

| 580–619 | ~16.5% | $860 | $16,600 |

How to Find Out Your Exact Score Range Right Now

The fastest way to know your current tier and track progress over time:

- Free FICO Score: Open the Experian app — shows your official FICO Score 8 from Experian, updated monthly, at no cost

- Free VantageScore: Credit Karma shows TransUnion and Equifax VantageScores, updated weekly

- Full credit report: AnnualCreditReport.com — free weekly reports from all three bureaus, no score included but full account and payment history

For the complete breakdown of every free credit score source and which one to use for each purpose, see our how to check your credit score for free guide.

Frequently Asked Questions

What is a good credit score in the USA?

In the USA, a “Good” credit score on the FICO scale is 670–739. Most lenders use 670 as the informal floor for standard credit products and 700 as the floor for competitive terms. Scores of 740+ are considered Very Good, and 800+ are Exceptional. Approximately 57% of Americans have a score of 700 or above.

What is the average credit score in the USA?

The average FICO score in the United States is approximately 718, placing the average American squarely in the “Good” tier. Average scores have risen steadily since the 2008 financial crisis, driven by improved consumer credit behavior and changes in bureau reporting practices including the removal of medical debt under $500 from reports.

How many points does a credit score go up each month?

There is no fixed monthly increase — credit scores respond to specific behavioral changes, not the passage of time alone. Reducing utilization from 60% to under 10% can add 40–60 points within one billing cycle. Making on-time payments consistently adds points gradually over 12–24 months. Time alone without behavioral change produces minimal score movement.

What is the lowest credit score possible?

The lowest possible FICO score is 300. In practice, scores below 400 are extremely rare — they typically require a combination of recent bankruptcy, multiple collection accounts, and complete absence of positive credit history. Most Americans with poor credit fall in the 500–579 range rather than approaching the floor of the scale.

Does your credit score reset after 7 years?

No — credit scores don’t reset. What happens at 7 years is that specific negative items (late payments, collections, charge-offs) are required by the Fair Credit Reporting Act to be removed from your credit report. When negative items are removed, the score typically improves — but the improvement depends on what else is on the report. If you’ve built positive history in the intervening years, the removal of old negative items combined with strong positive history can produce a significant score jump.

Final Thoughts

A credit score is a snapshot of a specific moment in your financial history. It changes every month — sometimes every week on VantageScore models — based on the information your creditors report.

The tiers matter because lenders use them as decision thresholds. The exact point value matters less than which side of 670, 700, or 740 you’re on. Knowing your tier tells you which products you can realistically target today and what behaviors will move you to the next one.

For the complete guide to fixing your credit score from any starting point, see our how to fix your credit score guide.

Disclaimer: FICO scoring models, lender rate tiers, and bureau reporting practices are subject to change. Interest rate examples are illustrative and based on general market conditions — actual rates vary by lender, loan type, and individual credit profile. This article is for educational purposes only.

Danilo is a Credit Analyst and the Founder of CreditPilotUSA.com. With deep expertise in the credit card industry, he translates complex banking news and reward systems into actionable financial strategies. Dedicated to helping Americans master their credit scores and maximize the cards in their wallets.