A bad credit score is not a life sentence. It is a math problem — and math problems have solutions.

Every number on the FICO scale between 300 and 579 got there through a specific combination of missed payments, high balances, collection accounts, or thin credit history. And every one of those factors is addressable. The timeline varies. The effort required varies. But the path is always the same: understand what’s pulling your score down, address those factors in order of impact, and let consistent positive behavior rebuild the number over time.

This guide covers the complete framework for fixing a bad credit score in the United States — from diagnosing the problem to implementing the right strategies in the right sequence — with links to deeper guides on every major topic.

Editorial note: CreditPilotUSA.com provides credit education based on FICO scoring methodology and federal consumer protection law. This article is for educational purposes only and does not constitute legal or financial advice.

Last updated: March 2026

Quick Answer

To fix a bad credit score in the USA: (1) check your credit report for free at AnnualCreditReport.com and identify every negative item, (2) dispute any inaccurate information with the credit bureaus, (3) pay down credit card balances to under 10% of your limit before each statement closes, (4) set autopay to ensure no future missed payments, and (5) open a secured credit card if you have no active accounts. Most people see measurable improvement within 60–90 days. Reaching “Good” credit (670+) from a poor starting point typically takes 12–24 months of consistent behavior.

Step 1: Know Exactly What You’re Fixing

You cannot fix a credit score without knowing what’s damaging it. The first action is always the same: pull your full credit report from all three bureaus and read every line.

You’re entitled to a free report from Equifax, Experian, and TransUnion at AnnualCreditReport.com — the only federally authorized source. Free weekly reports are currently available from all three bureaus.

What to look for on each report:

Negative items: Late payments, collections, charge-offs, bankruptcies, foreclosures. Note the date of each — this determines how long each item remains on your report and how much scoring weight it still carries. Items from 4–6 years ago carry significantly less weight than items from the last 12 months.

Errors: One in five American credit reports contains an error significant enough to affect the score. Look for accounts you don’t recognize, incorrect delinquency dates, duplicate collection entries for the same debt, and balances that haven’t been updated after being paid. Any inaccurate item can be disputed and removed.

Utilization: For every open credit card, calculate your current balance ÷ credit limit. If any individual card exceeds 30% — or your total across all cards exceeds 30% — utilization is likely one of your primary score-damaging factors.

Thin file signals: If you have fewer than 3 open accounts or your oldest account is under 2 years old, the score may be low not because of negative events but because the file doesn’t have enough positive history for a strong calculation.

To understand how to access your report and what each section means, see our complete guide on how to check your credit score for free.

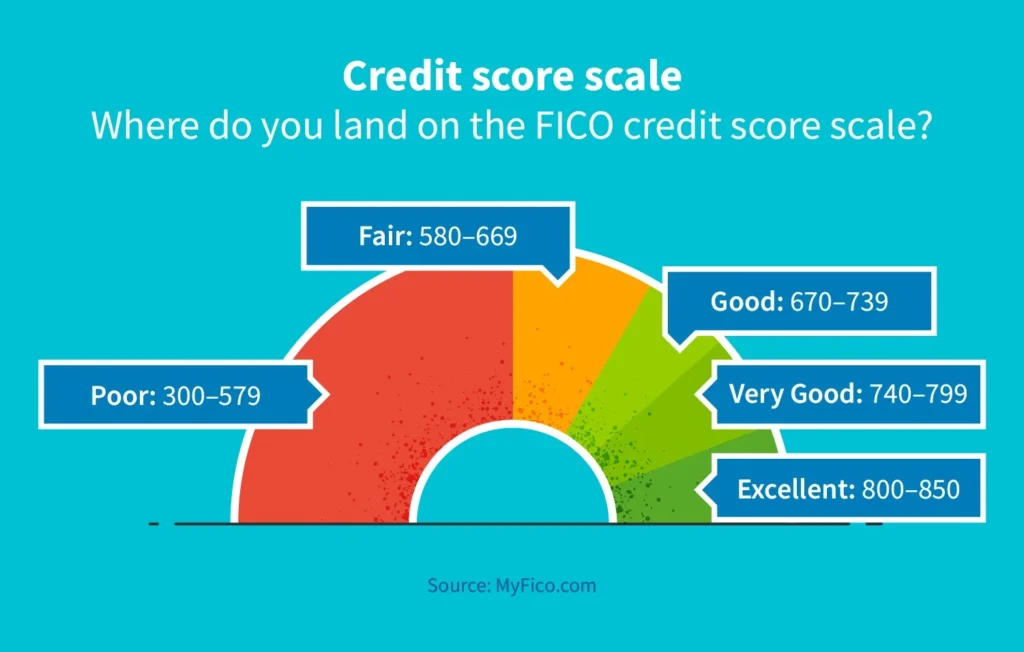

Step 2: Understand Your Score Range and What It Means

Before fixing a score, you need to know what range you’re in and what each tier means for your financial life — because the right strategy at 520 is different from the right strategy at 620.

| FICO Range | Category | Credit Card Access | Loan Terms |

|---|---|---|---|

| 800–850 | Exceptional | All cards, best terms | Best available rates |

| 740–799 | Very Good | Nearly all cards | Very competitive rates |

| 670–739 | Good | Most mainstream cards | Standard rates |

| 580–669 | Fair | Limited rewards cards | Higher rates |

| 300–579 | Poor | Secured cards only | Very limited access |

Understanding where you sit — and what the next threshold unlocks — gives the score-building process a concrete target. For the complete breakdown of what each range means for approvals, interest rates, and financial opportunities, see our guide on credit score ranges explained.

Step 3: Dispute Every Error Before Doing Anything Else

If your report contains inaccurate information, disputing it is the highest-leverage action available — because it can remove negative items entirely, with no waiting period.

Under the Fair Credit Reporting Act (FCRA), the credit bureaus must investigate any disputed item within 30 days. If they cannot verify the information with the original creditor, they must remove it. A single successful dispute on a significant negative item — a collection, a charge-off, a late payment with the wrong date — can add 20–50 points within 30–45 days.

How to dispute:

- File directly with each bureau reporting the error — Equifax, Experian, and TransUnion each have online dispute portals

- Provide your supporting documentation — statement copies, payment receipts, or simply a written explanation if the account is not yours

- Track the investigation — bureaus must respond within 30 days (45 days if you submitted via AnnualCreditReport.com)

What can and cannot be disputed: Accurate negative information — a real late payment, a legitimate collection — cannot be removed through a dispute. Only inaccurate or unverifiable items qualify. Credit repair companies that promise to remove accurate negative items are not providing a service the law permits.

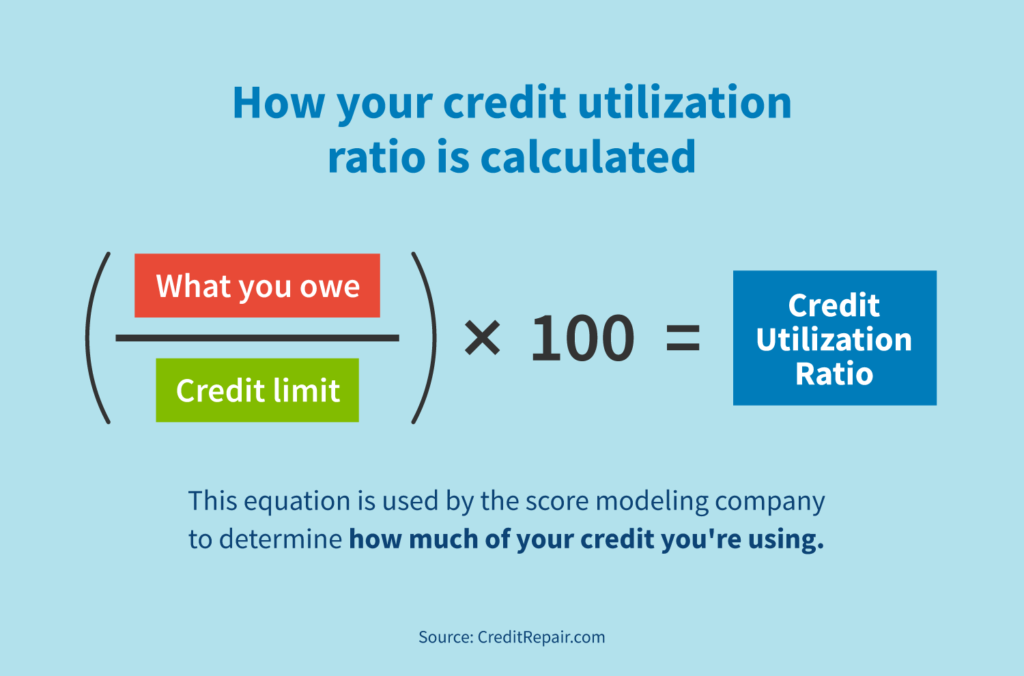

Step 4: Attack Credit Utilization First

If your report is accurate and your score is low, credit utilization is almost always a primary factor — and it’s the fastest legitimate lever available.

Credit utilization accounts for 30% of your FICO score. It measures the ratio of your reported credit card balances to your available credit limits. The lower the ratio, the higher the score contribution.

The key insight most Americans miss: utilization is calculated based on the balance reported on your statement closing date — not your payment due date. If your statement closes with a $800 balance on a $1,000 card, the bureaus see 80% utilization even if you pay it in full two weeks later.

The fix: Pay your balance down to under 10% of your credit limit before your statement closes each month. At $1,000 limit, that means keeping your balance under $100 at statement close. This single change can add 30–60 points within one billing cycle for cardholders currently carrying high balances.

For the complete mechanics of how utilization is calculated, why the statement date matters, and how to reduce it efficiently across multiple cards, see our full guide on what is credit utilization and how it affects your score.

Step 5: Stop the Bleeding — Never Miss Another Payment

Payment history is 35% of your FICO score — the single largest factor. Every on-time payment adds to the positive side of the ledger. Every missed payment does damage that takes years to fully recover from.

If you are currently missing payments, this is the first behavior to fix — before anything else. A new late payment on an already-damaged profile is one of the hardest setbacks to overcome because it resets the “most recent derogatory event” clock that scoring models use to weight negative history.

Two-action system: Set autopay for the minimum payment on every open account. This guarantees the bureau never sees a missed payment regardless of what else is happening in your life. Then pay the full balance manually before the statement closes — autopay is the safety net, early payment is the optimization.

Step 6: Add Positive History If Your File Is Thin

If your score is low because you have little credit history — rather than because of specific negative events — the solution is adding accounts that report positive payment history to all three bureaus.

Three options ranked by speed and accessibility:

Secured credit card: Deposit $200–$2,500 as collateral, which becomes your credit limit. The card reports monthly to all three bureaus like any other credit card. The Discover it Secured ($0 annual fee, automatic graduation review at 7 months) and Capital One Platinum Secured ($49–$200 deposit for $200 limit) are the strongest options at this tier. For the full comparison across score ranges, see our how to get approved for your first credit card guide.

Authorized user: Ask a family member or trusted friend with good credit to add you as an authorized user on their oldest, lowest-utilization credit card. The entire payment history of that account can appear on your report within one billing cycle — sometimes adding years of positive history overnight. You don’t need to use or even possess the card.

Credit-builder loan: Products like Self Financial allow you to make monthly payments into a savings account while the payment history is reported to all three bureaus. No deposit required upfront — the savings accumulate as you pay. After 12 months, most credit-builder loan users have both an established FICO score and $1,000–$1,800 in savings.

Step 7: Manage the Negative Items Already on Your Report

Beyond disputing errors, there are limited but legitimate ways to address accurate negative items before their statutory reporting window expires.

Goodwill deletion: For isolated late payments with an otherwise strong history, write a formal letter to the original creditor explaining the circumstances and requesting removal as a goodwill gesture. This is not legally required — the creditor can decline — but many do remove one-off late payments for long-standing customers with a clean track record otherwise. The letter must go to the original creditor, not the credit bureau.

Pay-for-delete: Some collection agencies will agree in writing to remove a collection account from your report in exchange for payment. This must be negotiated and documented in writing before payment is made. It is not universally available and major bureaus have discouraged the practice — but it remains a legitimate negotiating tool with some agencies.

Waiting with active rebuilding: For items that cannot be disputed or removed early, the most effective strategy is building strong positive history that outweighs the aging negative items. A charge-off from 4 years ago carries a fraction of the scoring weight it did at 6 months. With consistent on-time payments and low utilization, scores routinely recover to 670+ before the negative items even fall off the report.

For the complete breakdown of how long each type of negative item stays on your report and when they must be removed, see our guide on how long does negative credit stay on your report.

Step 8: Monitor Progress and Catch New Problems Early

Fixing a credit score is not a one-time action — it’s an ongoing process that requires monthly monitoring to confirm the strategy is working and catch new problems before they compound.

Two free tools for ongoing monitoring:

Credit Karma — shows VantageScore from TransUnion and Equifax, updated weekly. Use it to track directional progress after each billing cycle and watch utilization changes reflect in near real time.

Experian app — shows your FICO Score 8 from Experian, updated monthly. This is the score most lenders use — the benchmark for mortgage pre-approvals, auto loans, and premium card applications.

For the full comparison of monitoring tools at every stage of credit building, see our best apps to improve your credit score guide.

How Long Does It Take to Fix a Bad Credit Score?

Timeline depends on the severity of the damage, but these are realistic benchmarks for consistent practitioners:

| Starting Score | Primary Issue | Target: 580 | Target: 650 | Target: 700 |

|---|---|---|---|---|

| 500–540 | High utilization only | 1–2 months | 6–9 months | 12–18 months |

| 500–540 | Recent missed payments | 6–12 months | 12–18 months | 18–24 months |

| 540–580 | Collections + high utilization | 3–6 months | 9–12 months | 15–20 months |

| 580–620 | Aging negatives + thin file | 3–6 months | 6–9 months | 12–15 months |

| 620–650 | Utilization + few negatives | 1–3 months | 3–6 months | 6–12 months |

The fastest recoveries consistently share two characteristics: utilization drops to under 10% immediately, and no new negative events occur during the rebuild period. The slowest recoveries are those where new missed payments are added during the process — which resets the scoring clock on recent negative history.

The Credit Score Fix — Cluster Guides

Each factor that affects your credit score has its own mechanics, timelines, and strategies. These guides go deeper on every major topic:

Credit Score Ranges Explained: What Each Number Really Means in 2026 Understand exactly what your current score means for approvals, interest rates, and financial opportunities — and what the next threshold unlocks.

Why Did My Credit Score Drop? 9 Reasons and How to Fix Each One Your score dropped and you’re not sure why. This guide covers every common cause — from new inquiries to utilization spikes to reporting errors — with the fix for each.

What Is Credit Utilization and How Does It Affect Your Score? The 30% factor most Americans manage wrong. Full mechanics of how utilization is calculated, why the statement date matters, and the fastest way to bring it down.

How Late Payments Affect Your Credit Score (And What to Do About It) One missed payment can drop a 750 score by 100 points. Here’s exactly how much damage different lateness levels cause, how long the impact lasts, and your options for removal.

How to Check Your Credit Score for Free in the USA (2026) Every free credit score source in the US — what score each one shows, which is closest to what lenders see, and how to monitor all three bureaus without paying anything.

Frequently Asked Questions

How long does it take to fix a bad credit score?

Timeline depends on the cause. If low utilization is the primary issue, scores can improve significantly within one billing cycle — sometimes 30–60 days. If the damage comes from missed payments, collections, or bankruptcies, meaningful recovery typically takes 12–24 months of consistent positive behavior. The fastest recoveries combine immediate utilization reduction with a complete stop to new negative events.

Can I fix my credit score myself without a credit repair company?

Yes — and in most cases, a credit repair company cannot do anything you cannot do yourself for free. Disputing errors with credit bureaus, negotiating goodwill deletions, managing utilization, and adding positive accounts are all actions any consumer can take independently. The only legitimate value a credit repair company provides is doing the legwork on disputes — which you can do through each bureau’s free online portal.

What is the fastest way to raise a bad credit score?

The fastest legitimate method is reducing reported credit utilization below 10% before your statement closes. This change can reflect in your score within one billing cycle — approximately 30 days. The second fastest is a successful dispute of an inaccurate negative item, which can add 20–50 points within 30–45 days of the bureau completing its investigation.

Does checking my own credit score hurt it?

No. Checking your own credit score or pulling your own credit report is a “soft inquiry” and has zero impact on your FICO score. Only “hard inquiries” — triggered when a lender pulls your credit as part of a formal application — affect your score, typically by 5–10 points per inquiry.

What credit score is considered bad in the USA?

FICO scores below 580 are generally considered “Poor” — the lowest tier on the standard FICO scale. Scores between 580–669 are “Fair.” Most lenders use 670 as the informal floor for standard credit products, and 700 as the floor for competitive terms on loans and the best rewards cards.

Final Thoughts

A bad credit score is the result of specific, identifiable events — and every one of those events has a countermeasure.

The process is not complicated. Check your report. Dispute errors. Reduce utilization. Stop missing payments. Add positive history. Monitor monthly. Repeat.

What makes credit recovery feel hard is not the complexity — it’s the time. The FICO algorithm rewards sustained behavior, not single actions. The cardholders who fix their credit fastest are the ones who implement the right habits in the first month and maintain them without interruption for 12–24 months.

Start with your free credit report today. Find out exactly what’s on it. Then work through this guide one step at a time.

For more credit strategies, card comparisons, and financial guides built for US consumers, visit CreditPilotUSA.com — your trusted co-pilot for navigating the world of credit.

Disclaimer: Credit score improvements vary based on individual credit profiles. FICO scoring models are proprietary and subject to change. Information provided is for educational purposes only and does not constitute legal or financial advice.

Danilo is a Credit Analyst and the Founder of CreditPilotUSA.com. With deep expertise in the credit card industry, he translates complex banking news and reward systems into actionable financial strategies. Dedicated to helping Americans master their credit scores and maximize the cards in their wallets.