At 600, something shifts.

You’re no longer at the floor of the credit system. You’ve crossed into the “Fair” FICO tier — and with that crossing comes a meaningful expansion in what’s available to you. The secured-card-or-nothing reality of the 500s starts to open up. Some unsecured cards become accessible. Rewards start to enter the picture.

600 is the first score range where you have real choices — not just the least-bad option among guaranteed-approval products.

This guide covers the best credit cards available to Americans with a 600 credit score in 2026, what to prioritize at this range, and the fastest path to the next tier.

Editorial note: CreditPilotUSA.com evaluates credit cards based on approval requirements, fee structure, and real credit-building value. Cards are selected independently.

Last updated: March 2026

Quick Answer

With a 600 credit score, you can access both secured and some unsecured credit cards. The best options are the Discover it® Secured ($0 fee, 2% cashback, automatic graduation), the Capital One Platinum (unsecured, $0 fee, designed for fair credit), and the Petal® 2 Visa (unsecured, $0 fee, 1–1.5% cashback, no late fees). All report to all three bureaus. At 600, prioritize cards with no annual fee, a path to unsecured credit, and consistent bureau reporting over any specific rewards rate.

What a 600 Credit Score Means for Card Approval

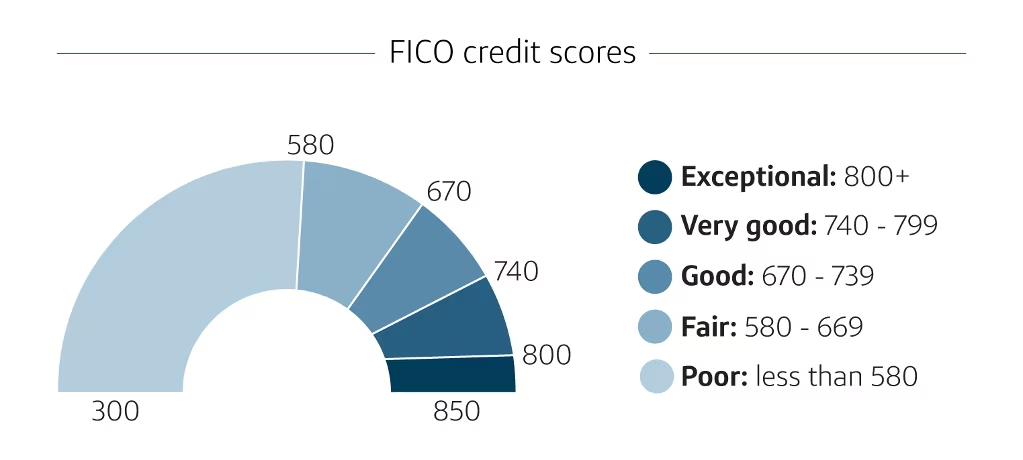

600 sits in the “Fair” tier (580–669) on the FICO scale. It’s a meaningful step above 550 — but still below the 670 threshold where mainstream approval becomes reliable.

What opens up at 600 vs. 550:

- Some unsecured cards from major issuers (Capital One Platinum, select Citi products)

- Fintech unsecured cards using alternative underwriting (Petal, Mission Lane)

- Better secured card terms — higher initial limits, faster graduation reviews

- Some store cards (retail credit cards with lower approval thresholds)

What’s still not reliably accessible at 600:

- Premium rewards cards (typically 700+)

- Travel cards

- Cards with strong welcome bonuses

- Low-APR products

The strategic priority at 600 is the same as at 550, just with more tools: add positive history, keep utilization under 10%, and reach 650–670 where the mainstream credit card market opens up.

For a broader view of bad-credit card options, see our how to get approved for your first credit card guide.

Best Credit Cards for 600 Credit Score

1. Discover it® Secured Credit Card

Best if you want the strongest graduation path

Even at 600 — where unsecured options start to exist — the Discover it Secured remains one of the strongest choices because of its automatic graduation review at 7 months. Cardholders who use it responsibly get upgraded to an unsecured card and receive their full deposit back, typically without a new application or hard inquiry.

Key details:

- Annual fee: $0

- Security deposit: $200–$2,500 (becomes credit limit)

- Cashback: 2% at gas stations and restaurants, 1% everywhere else

- Cashback Match: All Year 1 earnings doubled automatically

- Graduation: Automatic review at 7 months

- Reports to: Equifax, Experian, TransUnion

Why it still makes sense at 600: The Cashback Match makes Year 1 the highest-earning period on any secured card at any tier. And the 7-month graduation path means a 600-score applicant could have an unsecured Discover card with their deposit returned within 9–12 months of opening.

2. Capital One Platinum Credit Card

Best unsecured option for 600 — $0 fee, no deposit

The Capital One Platinum is specifically designed for the fair credit range (580–669) and is one of the most accessible unsecured cards available at 600. No deposit required, no annual fee, and an automatic credit limit review after 6 months.

Key details:

- Annual fee: $0

- Security deposit: None — fully unsecured

- Credit check: Yes (hard inquiry)

- Credit limit increase: Automatic review after 6 months

- Reports to: Equifax, Experian, TransUnion

- Rewards: None — pure credit-building product

Why it matters: Getting approved for an unsecured card at 600 is a milestone. The Platinum adds an unsecured revolving account to your profile — a signal to scoring models that a major issuer trusts you without collateral. Paired with a secured card, it diversifies your credit mix and accelerates score building.

The tradeoff: No rewards, no perks. The Capital One Platinum is purely a credit-building instrument. Use it for one small purchase per month, pay in full, and don’t expect it to earn anything beyond score improvement.

3. Petal® 2 “Cash Back, No Fees” Visa® Credit Card

Best unsecured card with rewards at 600

Petal uses its own Cash Score™ underwriting — evaluating banking history, income, and spending patterns alongside or instead of FICO. This allows some 600-range applicants to qualify for an unsecured card with real rewards and genuinely zero fees.

Key details:

- Annual fee: $0

- Late fee: $0

- Foreign transaction fee: $0

- Security deposit: None — unsecured

- Cashback: 1% immediately, rising to 1.5% after 12 months of on-time payments

- Credit limit: $300–$10,000 based on Cash Score™

- Reports to: Equifax, Experian, TransUnion

The caveat: Petal 2 approval is not guaranteed for all 600-score applicants. Clean banking history (no overdrafts, consistent income deposits) significantly improves approval odds. For applicants with clean bank records but imperfect FICO scores, this is the best unsecured rewards card available at this tier.

4. Capital One QuicksilverOne Cash Rewards

Best for earning rewards while rebuilding at 600

The QuicksilverOne is Capital One’s rewards card for the fair credit range — and it earns 1.5% cashback on every purchase with no category restrictions.

Key details:

- Annual fee: $39

- Cashback: 1.5% on every purchase

- Foreign transaction fee: $0

- Credit limit increase: Automatic review after 6 months

- Reports to: Equifax, Experian, TransUnion

The math on the annual fee: At $39/year, you need $2,600 in annual spending at 1.5% to break even ($2,600 × 1.5% = $39). For cardholders spending $300+/month through the card, the QuicksilverOne earns more than it costs. Below $200/month, the Capital One Platinum ($0 fee) is a better choice.

Best for: Cardholders at 600 spending $300+/month who want real cashback during the rebuilding phase without waiting for a premium card.

5. Mission Lane Visa® Credit Card

Best for applicants declined by Capital One and Discover

Mission Lane is an unsecured card designed specifically for the fair credit range — and it approves some applicants who have been declined by major issuers. It uses flexible underwriting and offers a pre-qualification tool with no hard inquiry.

Key details:

- Annual fee: $0–$59 (determined at application)

- Security deposit: None — unsecured

- Cashback: 1.5% on all purchases (on qualifying accounts)

- Credit limit: $300–$2,000

- Reports to: Equifax, Experian, TransUnion

Best for: Applicants at 600 who have been declined by Capital One and Discover and need an unsecured fallback option. Check pre-qualification first to see your specific offer before submitting a hard inquiry.

The Priority Stack at 600

At this score range, the fastest path to 650+ involves three concurrent actions:

Keep reported utilization under 10% across all cards. This is the highest-leverage action available. If you have a $500 total credit limit across cards, keep your total reported balance under $50. Pay down before statement close each month. For the exact mechanics, see our credit score payment strategy guide.

Don’t open more than one new account in the first 6 months. Each hard inquiry costs 5–10 points and each new account lowers your average account age. The score impact of two simultaneous new accounts often delays progress more than it accelerates it.

Target the automatic upgrade reviews. Capital One reviews at 6 months. Discover reviews at 7 months. These upgrades — which increase your credit limit without a new hard inquiry — are the most efficient way to lower utilization as your score builds.

What Opens Up at 650

Crossing 650 is the next meaningful threshold. At 650+:

- Discover it® Cash Back (unsecured, 5% rotating categories) becomes accessible

- Chase Freedom Rise® (unsecured, 1.5% everywhere) becomes accessible

- Some balance transfer cards become available

- Personal loan rates improve materially

For the full picture of what’s available at 650, see our credit cards for 650 credit score guide. And for the 500–700 rebuild roadmap, see our improve credit score 500 to 700 guide.

Frequently Asked Questions

What credit cards can I get with a 600 credit score?

With a 600 credit score, you can access both secured cards (Discover it Secured, Capital One Platinum Secured) and some unsecured cards (Capital One Platinum, Petal 2, Capital One QuicksilverOne). The best choice depends on whether you can provide a deposit: if yes, the Discover it Secured offers the strongest graduation path; if not, the Capital One Platinum is the most accessible unsecured option.

Is 600 a good credit score?

600 falls in the “Fair” FICO tier (580–669), which is above “Poor” (300–579) but below “Good” (670–739). At 600 you can access some credit products, but you’ll face higher APRs and lower credit limits than borrowers at 670+. Most premium rewards cards, travel cards, and low-APR products require 670–700 or above.

How can I raise my credit score from 600 to 650?

The fastest path from 600 to 650 involves keeping reported utilization under 10% (pay before statement close, not just before due date), making every payment on time (35% of FICO score), and avoiding new hard inquiries for at least 6 months. Most cardholders implementing these habits consistently reach 650 within 6–9 months from a 600 starting point.

Final Thoughts

At 600, you have real options for the first time. The goal now is to use them strategically — pick one or two cards, manage utilization tightly, and let the positive history compound.

The difference between 600 and 670 is typically 12–18 months of consistent behavior, not years of waiting. The right card choices at this stage are the fastest way to make that timeline shorter.

For the full landscape of options below 600, see our how to get approved for your first credit card guide. For what opens up above 650, see our credit cards for 650 credit score guide.

Disclaimer: Approval is not guaranteed and depends on individual credit profiles and issuer criteria. Card terms and features are subject to change. This article is for educational purposes only.

Danilo is a Credit Analyst and the Founder of CreditPilotUSA.com. With deep expertise in the credit card industry, he translates complex banking news and reward systems into actionable financial strategies. Dedicated to helping Americans master their credit scores and maximize the cards in their wallets.