Most Americans check their credit score the same way they check their blood pressure: only when something feels wrong. By then, the damage is already done.

The good news? There’s an entire category of apps built specifically to flip this dynamic — tools that monitor your score in real time, explain exactly what’s dragging it down, and give you a concrete action plan to push it higher. Some of them are completely free. A few are so effective that users report gaining 50 to 100 points within a single year of consistent use.

The best apps to improve your credit score don’t just show you a number. They show you why your number is what it is — and what to do about it tomorrow morning. This guide covers the top options available in 2026, what makes each one worth downloading, and the strategies that actually move the needle.

Why Most People’s Credit Score Is Lower Than It Should Be

Before we get into the apps, let’s be clear about something: most people with a “fair” credit score don’t have a spending problem. They have an information problem.

They don’t know their utilization is sitting at 67%. They don’t know a medical bill from three years ago went to collections and is silently pulling their score down. They don’t know that closing a credit card last year shortened their average account age by four years.

These are fixable problems — but only if you can see them. Credit score apps exist to make the invisible visible. And in 2026, they’ve gotten remarkably good at it.

What the Best Credit Score Apps Actually Do

Not all credit score apps are created equal. The best ones go far beyond showing you a three-digit number. Here’s what separates genuinely useful apps from marketing tools dressed up as financial help:

Real-time score monitoring — alerts you the moment your score changes, so you know within 24–48 hours when something affects your credit file

Factor analysis — breaks down exactly which elements are helping or hurting your score, with specific percentages and actionable explanations

Dispute tools — some apps let you flag and dispute errors on your credit report directly from the app, without having to navigate bureau websites

Credit building features — a growing number of apps include built-in credit builder products — secured cards, credit builder loans, or rent reporting — that directly add positive history to your file

Score simulators — let you model “what if” scenarios before you act: what happens to my score if I pay off this card? If I open a new account? If I close my oldest card?

Personalized recommendations — suggest specific financial products (cards, loans) that match your current credit profile and are likely to approve you

The 8 Best Apps to Improve Your Credit Score in 2026

🥇 Credit Karma

Best free all-in-one credit monitoring app

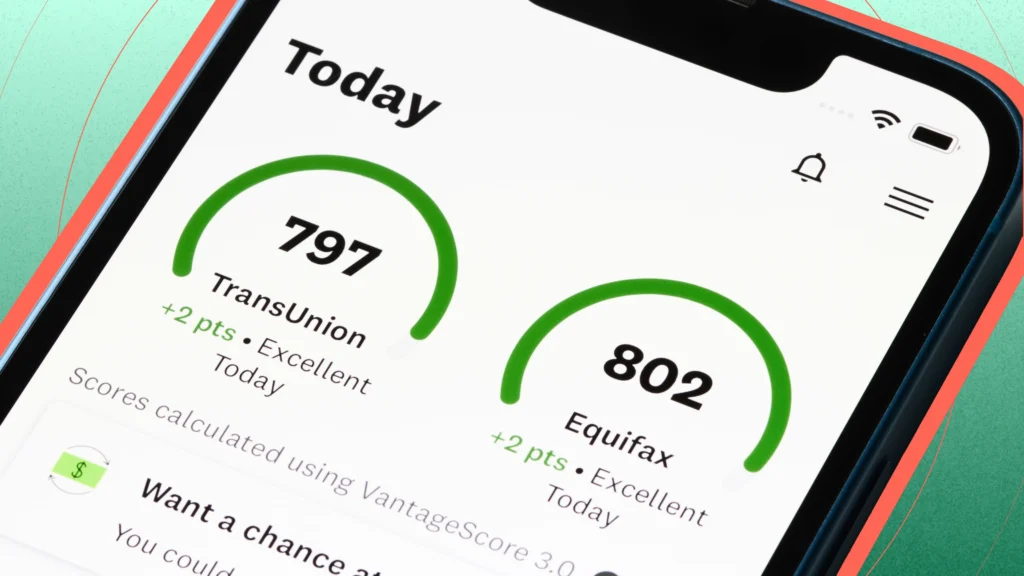

Credit Karma remains the most widely used credit score app in the United States — and for good reason. It gives you free VantageScore 3.0 scores from both TransUnion and Equifax, updated weekly, with detailed factor breakdowns and personalized recommendations.

What it does well:

- Free weekly score updates from two bureaus

- Detailed credit report breakdown with clear explanations

- Credit monitoring alerts for new accounts, hard inquiries, and score changes

- Tax filing integration (Credit Karma Tax)

- Personalized card and loan recommendations based on your actual profile

- Dispute Center for flagging report errors

What to keep in mind: Credit Karma shows VantageScore, not FICO. Your score here may differ by 10–50 points from what a lender pulls. Use it to track trends and catch issues — not as your definitive score.

Cost: Free Best for: Anyone who wants comprehensive credit monitoring at zero cost

🥈 Experian

Best for official FICO Score access — free

Experian’s app is the only major free credit monitoring tool that gives you access to your actual FICO® Score 8 — the score 90% of top lenders use when making credit decisions. This alone makes it uniquely valuable for anyone preparing to apply for a mortgage, car loan, or premium credit card.

What it does well:

- Free FICO® Score 8 updated monthly

- Full Experian credit report access

- Experian Boost™ — the standout feature: adds on-time utility, phone, and streaming payments (Netflix, Spotify, Disney+) to your Experian credit file, potentially raising your score immediately

- Real-time fraud alerts and dark web monitoring

- Credit lock to prevent unauthorized account openings

What to keep in mind: Experian Boost only affects your Experian file, not TransUnion or Equifax. The score increase from Boost is real but varies — some users gain 10–20 points; others see minimal change depending on their existing profile.

Cost: Free (Experian CreditWorks Premium available at $24.99/month for three-bureau monitoring) Best for: Anyone preparing to apply for credit — this is the score lenders actually see

🥉 myFICO

Best for serious credit builders who need lender-accurate scores

If you’re within 6–12 months of a major financial decision — buying a home, financing a car, applying for a business loan — myFICO gives you the most complete picture of exactly what lenders will see.

What it does well:

- Access to 28 versions of your FICO score across all three bureaus — including the specific scores used by mortgage, auto, and card lenders

- Three-bureau credit reports with side-by-side comparison

- Score simulator to model the impact of financial decisions before making them

- Identity theft protection and $1 million in insurance coverage

- Detailed explanation of what’s driving each score variant

What to keep in mind: myFICO is a premium service — not the right tool for casual monitoring. It’s specifically valuable for people who need to know precisely what a mortgage underwriter will see when they pull your credit next month.

Cost: $19.95–$39.95/month depending on plan Best for: Pre-mortgage applicants, serious credit builders, anyone preparing for a major loan

💳 Self — Credit Builder

Best app for people building credit from scratch

Self takes a completely different approach. Instead of just monitoring your credit, it actively builds it through a credit builder loan — a financial product specifically designed to create positive payment history on your credit report.

How it works:

- You open a credit builder account and make fixed monthly payments ($25–$150/month)

- Self holds the money in a certificate of deposit while you pay

- Every payment is reported to all three major credit bureaus as an installment loan

- At the end of the term (12 or 24 months), you receive the savings back minus interest and fees

- You can also qualify for a Self Visa® Secured Credit Card once you’ve built $100 in savings

What it does well:

- Builds both payment history (35% of FICO) and credit mix (10%) simultaneously

- No credit check required to open an account

- Reports to Equifax, Experian, and TransUnion every month

- Savings component means you’re building an emergency fund while building credit

- Users report average score increases of 32–49 points within the first year

Cost: Monthly fees range from $25–$150 depending on plan; interest applies Best for: People with no credit history, thin credit files, or recovering from bankruptcy

🔍 Chime Credit Builder

Best for building credit with no fees and no interest

Chime’s Credit Builder is one of the most beginner-friendly credit building tools available — and one of the few with no interest charges and no minimum deposit requirement.

How it works:

- Move money from your Chime spending account into your Credit Builder secured account

- Use the Credit Builder Visa® card for everyday purchases

- Chime pays the balance automatically at the end of each month using your secured funds

- Every on-time payment is reported to all three bureaus

What it does well:

- No credit check, no hard inquiry to open

- No annual fee, no interest, no minimum security deposit

- Automatic payment eliminates the risk of missed payments

- Seamlessly integrated with Chime’s banking app

- Members report average credit score increases of 30 points within 8 months

Cost: Free (requires a Chime spending account) Best for: True beginners and anyone who wants to build credit with zero financial risk

📊 Credit Sesame

Best for identity theft protection + credit monitoring combo

Credit Sesame provides free TransUnion VantageScore monitoring combined with robust identity protection features that are increasingly important as data breaches become more common.

What it does well:

- Free monthly credit score updates with factor analysis

- $1 million identity theft insurance included at no cost

- Sesame Cash — a debit account with credit-building features built in

- Personalized savings recommendations based on your credit profile

- Credit score simulator for modeling financial decisions

Cost: Free (Platinum plan at $9.95/month for enhanced features) Best for: Anyone prioritizing identity protection alongside credit monitoring

🏠 Rental Kharma / RentReporters

Best for renters who want credit for on-time rent payments

This is one of the most underused credit-building strategies in America: you’re already paying rent every month — most of you aren’t getting credit for it.

Rental Kharma and RentReporters are specialized apps that report your rent payment history to the major credit bureaus, adding a significant positive payment history that most renters never receive.

What it does well:

- Reports up to 24 months of past rent payments retroactively

- Adds a consistent monthly installment-like entry to your credit file

- Average reported score increase of 35–40 points within 3 months

- No landlord participation required for some reporting services

Cost: Rental Kharma: $75 enrollment + $8.95/month | RentReporters: $94.95/year Best for: Long-term renters with thin credit files who want to leverage existing payment history

📱 Kikoff

Best micro credit builder for absolute beginners

Kikoff offers one of the simplest credit-building products available: a $750 revolving credit line used only to purchase items from Kikoff’s store, reported monthly to Equifax and Experian.

What it does well:

- Instant approval — no credit check, no hard inquiry

- $750 credit limit improves your available credit immediately

- Monthly reporting builds payment history passively

- App interface is clean and beginner-friendly

- Consistent monthly fee — predictable and transparent

Cost: $5/month Best for: Absolute beginners who want the simplest possible entry point into credit building

All 8 Apps — Quick Comparison

| App | Score Type | Cost | Best Feature | Best For |

|---|---|---|---|---|

| Credit Karma | VantageScore (2 bureaus) | Free | Full monitoring + recommendations | Everyone |

| Experian | FICO® Score 8 | Free | Experian Boost™ | Pre-applicants |

| myFICO | 28 FICO versions | $19–$40/mo | Mortgage-ready scores | Pre-mortgage |

| Self | Builds credit | $25–$150/mo | Credit builder loan | No credit history |

| Chime | Builds credit | Free | No fees, no interest | True beginners |

| Credit Sesame | VantageScore | Free | $1M identity insurance | Identity protection |

| Rental Kharma | Builds credit | $9/mo | Rent reporting | Renters |

| Kikoff | Builds credit | $5/mo | Instant $750 credit line | Absolute beginners |

The Strategy That Compounds All of These Apps

Using one app is good. Using the right combination is where the real results happen.

The Beginner Stack (score: 0–580): Chime Credit Builder + Kikoff + Rental Kharma → Builds payment history, adds revolving and installment credit, reports rent — all simultaneously, for under $15/month total

The Rebuilder Stack (score: 580–669): Credit Karma + Experian (with Boost) + Self → Monitor from two angles, add utility payments to your Experian file, and layer in a credit builder loan for installment diversity

The Optimizer Stack (score: 670–749): Experian + myFICO + Credit Karma → Track your real FICO score, simulate the impact of financial decisions, and monitor all three bureaus for errors and fraud

The Pre-Mortgage Stack (score: 750+): myFICO + Experian → See exactly what your mortgage lender will see, across all three bureaus, using all relevant FICO score versions

The Habits That Make These Apps Actually Work

No app improves your credit score on its own. They’re tools — and tools only work when used consistently. Pair any of these apps with these four habits and your score will move:

Pay every bill on time, every month. Payment history is 35% of your FICO score. One missed payment can undo months of progress. Set up autopay on every account and let the apps monitor the results.

Keep your credit card balances below 10%. Utilization is 30% of your score. Most people target 30% — the real high-scorers target 10% or lower. Use your credit monitoring app to check your reported utilization before your statement closes each month.

Dispute every error you find. According to the Consumer Financial Protection Bureau (CFPB), credit report errors are more common than most people realize. Use Credit Karma’s Dispute Center or Experian’s dispute portal to flag anything inaccurate. A single corrected error can raise your score 20–50 points. For a full guide on what errors to look for, see our article on common credit score mistakes.

Check your score monthly — not obsessively. Weekly or monthly monitoring through a free app is healthy and productive. Checking daily creates anxiety without additional insight. Set a recurring monthly calendar reminder, review your score and factors, and adjust your behavior accordingly. For your official full credit reports from all three bureaus, visit AnnualCreditReport.com — the only federally authorized source — at least once a year.

What a Good Target Score Looks Like

If you’re new to credit monitoring, it helps to know what you’re working toward. In the United States, a good credit score starts at 670 on the FICO scale — the threshold where most mainstream credit cards, auto loans, and apartment applications open up. A score above 740 is considered “very good” and unlocks the best interest rates on the market.

For a complete breakdown of every credit score range and what each tier means for your financial life, see our What Is a Good Credit Score in the USA guide.

And if you’re ready to add a credit card to your credit-building strategy, our Best Credit Cards for Beginners guide walks you through every option available to first-time applicants.

Final Thoughts

The gap between the credit score you have and the credit score you deserve is almost always an information gap — and in 2026, there’s no excuse for not having that information. The best apps to improve your credit score are free, powerful, and available on your phone right now.

Download Credit Karma to start monitoring. Add Experian for your real FICO score and the Boost feature. If you’re building from scratch, layer in Chime or Self. If you’re a renter, activate Rental Kharma and get credit for what you’re already paying.

Start today. Your score six months from now will reflect exactly how much attention you paid to it right now.

For more guides on credit building, card comparisons, and financial strategies built for real Americans, visit CreditPilotUSA.com — your trusted co-pilot for navigating the world of credit.

Disclaimer: App features, pricing, and availability are subject to change. Information provided is for educational purposes only and does not constitute financial advice.

Danilo is a Credit Analyst and the Founder of CreditPilotUSA.com. With deep expertise in the credit card industry, he translates complex banking news and reward systems into actionable financial strategies. Dedicated to helping Americans master their credit scores and maximize the cards in their wallets.