Having bad credit doesn’t mean you’re out of options. In 2026, the best credit cards for bad credit are designed to help you rebuild your FICO score while providing a financial safety net.

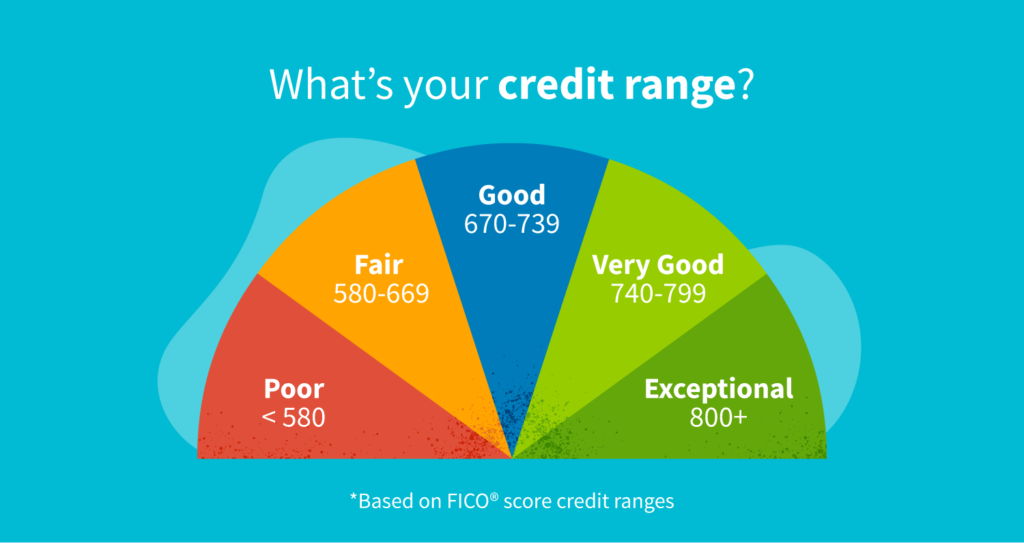

Whether you’re recovering from bankruptcy, medical debt, or missed payments, choosing a card that reports to all three bureaus (Equifax, Experian, and TransUnion) is the only way to move from a sub-580 score to the 700s.

| Best For… | Card Recommendation | Top Advantage |

| No Credit Check | OpenSky® Secured Visa® | No bank account required to apply |

| Highest Approval | Chime Credit Builder Visa® | No interest, no fees, no credit check |

| No Deposit | Credit One Bank® Platinum | Unsecured card for poor credit |

| Best Rewards | Discover it® Secured | Earn cashback while rebuilding |

What is The Easiest Credit Card to Get With Bad Credit?

The easiest credit cards to get with bad credit in 2026 are Secured Credit Cards like the OpenSky® Secured Visa® or the Chime Credit Builder Visa®. These cards have near-guaranteed approval because they either require a security deposit or don’t perform a traditional credit check, making them perfect for those with scores below 580.

How Credit Cards for Bad Credit Help You Rebuild

Credit cards for bad credit are financial products designed for consumers with a FICO score below 580 — often called “poor” or “damaged” credit. These cards have lenient approval requirements and are structured to help borrowers rebuild their credit history.

They typically come in two forms:

- Secured credit cards — require a refundable security deposit (usually $200–$500) that acts as your credit limit. This deposit is returned to you once you upgrade or close the account in good standing.

- Unsecured credit cards for bad credit — no deposit required, but often carry higher fees and lower credit limits

Both types report your payment activity to Equifax, Experian, and TransUnion each month, which is exactly how your credit score gets rebuilt over time.

Note: Not all unsecured cards for bad credit are created equal. Some carry high ‘program fees’ that can eat into your credit limit before you even use the card. Always prioritize cards with no monthly maintenance fees when possible.

How Credit Cards for Bad Credit Work in the United States

In the US, your credit score is calculated by FICO based on five key factors. When you use a bad credit card responsibly, you’re directly improving the most important ones.

Here’s how the process works:

- You apply for a secured or unsecured card designed for poor credit

- You get approved — most of these cards have flexible criteria or pre-qualification tools

- You make small purchases — everyday spending like groceries, gas, or a streaming subscription

- You pay on time, in full — this is the single most powerful action you can take

- The issuer reports your positive payment history to all three credit bureaus monthly

- Your credit score rises — most users see measurable improvement within 3–6 months

- You graduate to a better card with higher limits and rewards after 12–18 months

The key insight: you don’t need to spend a lot or carry a balance. You simply need consistent, on-time payments on a small balance.

Step-by-Step Guide: How to Rebuild Credit With a Bad Credit Card

Follow these seven steps to get the best results from your first card:

- Check your credit score for free — Use AnnualCreditReport.com to pull your full report and dispute any errors before applying.

- Choose the right card type — If you have a 500–579 score, go secured; below 500 or no score, consider OpenSky or Chime (no credit check required).

- Apply for one card only — Multiple applications trigger hard inquiries and lower your score further

- Set your credit limit strategically — For secured cards, deposit only what you can afford; start with $200–$300.

- Use the card for one or two small recurring bills — Keeping a small balance (under 10% utilization) is often better for your score than paying it to $0 before the statement closes.

- Set up autopay for the full statement balance — This prevents late payments automatically and avoids interest charges.

- Monitor your score monthly — Use Credit Karma or Experian’s free monitoring to track your progress and stay motivated.

What Affects Your Approval Odds?

Understanding what drives approval and credit growth helps you make smarter decisions:

- Payment history (35% of FICO score) — The single biggest factor; one missed payment can drop your score 60–100 points

- Credit utilization (30%) — Keep spending below 30% of your limit; below 10% is ideal for fast score growth

- Length of credit history (15%) — Don’t close your first card; keeping it open increases your average account age

- Credit mix (10%) — Having both a credit card and an installment loan (like a credit builder loan) boosts your score faster

- New credit inquiries (10%) — Each application creates a hard inquiry; space out applications by at least 6 months

- Deposit requirements — Lower deposits make secured cards more accessible but also mean lower initial credit limits

- Annual fees — Some bad credit cards charge $75–$99/year; factor this into your decision

Best Credit Cards for Bad Credit: Top Picks at a Glance

| Card | Type | Annual Fee | Deposit Required | Best For |

|---|---|---|---|---|

| Discover it® Secured | Secured | $0 | $200 min | Cash back + rebuilding |

| Capital One Platinum Secured | Secured | $0 | $49–$200 | Low deposit |

| OpenSky® Secured Visa® | Secured | $35 | $200 min | No credit check |

| Credit One Bank® Platinum Visa® | Unsecured | $75 | None | No deposit needed |

| Chime Credit Builder | Secured | $0 | No minimum | No hard inquiry |

| Indigo® Mastercard® | Unsecured | $0–$99 | None | Post-bankruptcy |

| Self Secured Visa® | Secured | $25 | Via loan | Savings + credit building |

Expert Note: Unlike some subprime lenders, every card in the table above reports to all three major credit bureaus (Equifax, Experian, and TransUnion), which is the only way to effectively rebuild your score in 2026.

Best Tips to Improve Results With a Bad Credit Card

Pay before the statement closing date. Your issuer reports your balance to the bureaus on the statement closing date — not the due date. Paying down your balance before this date lowers your reported utilization.

Request a credit limit increase after 6 months. A higher limit reduces your utilization ratio automatically, even if your spending stays the same.

Add a co-signer or become an authorized user. If a family member has good credit, being added to their account can boost your score while you build your own.

Mix in a credit builder loan. Products like Self or a local credit union’s credit builder loan add an installment account to your file — FICO rewards a healthy credit mix.

Dispute errors on your credit report. According to the Consumer Financial Protection Bureau (CFPB), errors on credit reports are more common than most people think. A single corrected error can raise your score by 20–50 points.

Common Mistakes to Avoid

- ❌ Applying for multiple cards at once — Each hard inquiry lowers your score; apply for one card and wait at least 6 months before the next

- ❌ Carrying a high balance — Even if you pay on time, a balance above 30% of your limit actively hurts your score every month

- ❌ Paying only the minimum — Minimum payments keep you in debt longer and cost you significantly in interest

- ❌ Closing old accounts — Closing your first card shortens your credit history and raises your overall utilization ratio

- ❌ Ignoring your credit report — Errors and fraudulent accounts go unnoticed without regular monitoring

- ❌ Choosing a card with excessive fees — Some predatory cards charge setup fees, monthly fees, and annual fees that consume your credit limit before you even swipe

- ❌ Missing the grace period — Even one 30-day late payment is reported to all three bureaus and can haunt your file for seven years

Expert Tips for Rebuilding Credit Faster

1. The “set it and forget it” method works best. Put one small recurring charge on your bad credit card — like a $10 streaming subscription — set up autopay for the full balance, and let it run. This creates perfect payment history with zero risk of overspending.

2. Target a utilization rate below 10%, not just 30%. Most financial coaches say 30% is the ceiling, but studies show that scores in the 750+ range typically have utilization below 10%. Aim lower to build faster.

3. Check for pre-qualification tools before applying. Most major issuers — including Capital One and Discover — offer soft-pull pre-qualification that tells you your approval odds without affecting your score. Always use these before submitting a full application.

4. Combine a secured card with a credit builder loan. Using both a revolving account (credit card) and an installment account (credit builder loan) at the same time is one of the fastest known methods to build a credit file from scratch or repair a damaged one.

5. Set a 12-month graduation goal. Mark your calendar for 12 months after opening your first bad credit card. At that point, check if you qualify for an unsecured card with no annual fee and real rewards. The goal is always to move up, not to stay with a high-fee product longer than necessary.

Not sure if you should get a cashback card instead? See our guide on the Best Cashback Credit Cards in the USA.

Frequently Asked Questions

What is the easiest credit card to get with bad credit in the USA?

The easiest credit cards to get with bad credit are the OpenSky® Secured Visa® (no credit check required) and the Chime Credit Builder Visa® (no hard inquiry). Both are accessible even if your score is below 500 or you have a bankruptcy on your file.

Can I get a credit card with a 500 credit score?

Yes. A 500 credit score falls in the “poor” range, but secured cards like the Capital One Platinum Secured and the Discover it® Secured are designed for scores in the 500–579 range. Some unsecured options like Credit One Bank® also approve applicants in this range.

Do bad credit credit cards help rebuild your score?

Yes, as long as you use them responsibly. Cards that report to all three major credit bureaus — Equifax, Experian, and TransUnion — will reflect your positive payment history each month. Most users see measurable score improvement within 3 to 6 months.

What’s the difference between guaranteed approval and easy approval credit cards?

Truly “guaranteed approval” cards don’t exist — all issuers have some criteria. However, near-guaranteed options like OpenSky (no credit check) come very close. “Easy approval” cards simply have more lenient requirements than standard cards. Always read the terms carefully before applying.

How long does it take to go from bad credit to good credit?

Most people can move from a poor score (below 580) to a fair or good score (670+) within 12 to 24 months of consistent responsible use. The exact timeline depends on your starting score, the severity of negative marks, and how diligently you manage your new account.

Final Thoughts

A bad credit score is not a life sentence — it’s a starting point. The best credit cards for bad credit give you the tools to prove your creditworthiness, one on-time payment at a time. Whether you start with a secured card, a no-check option, or a credit builder combo, the most important step is to begin.

Stay consistent, keep your balances low, and revisit your options every 12 months. Your future self — with a 700+ score and access to premium financial products — will thank you for starting today.

For more guides on credit cards, credit score strategies, and personal finance tips tailored to US consumers, visit CreditPilotUSA.com — your trusted co-pilot for navigating the world of credit.

Disclaimer: Credit card terms, fees, and approval criteria are subject to change. Always verify current conditions directly with the card issuer before applying.

Danilo is a Credit Analyst and the Founder of CreditPilotUSA.com. With deep expertise in the credit card industry, he translates complex banking news and reward systems into actionable financial strategies. Dedicated to helping Americans master their credit scores and maximize the cards in their wallets.